When I was a teenager I always thought I would either end up in accounting like my dad, or in a medical profession like my mom. We really limit ourselves to the choices we see around us sometimes, but thankfully, the more adventurous side of me chose to take neither of those paths.

It has been over a decade since I ever considered a career in accounting and finance and I have once again made it a subject of concern. Except now I am very certain that I am fine with my career as a software engineer. As I inevitably have to make the right financial decisions for my family that only currently consists of my dog, my wife, and I, I figured I might as well do it good enough to never have to let down my little family.

My exploration on this journey to better finance really started like many other interests I have; by using a software application that poked my curioty and sparked my interest. For this, it was Debit & Credit macos desktop app. Before this app I had seen finance nerds share spreadsheets among each other and that just didn’t seem fascinating enough for me. I couldn’t edit a spreadsheet file without breaking a formula or worse.

A friend had recommended Mint to me a long time ago and I gave it a try. I think Mint is a beautifully designed application with some cool integrations to link your bank accounts and various scheduled payment accounts which it then uses to spit out graphs and charts to show your spending habits. The problem I had with Mint was that it was so cool that it fed into my laziness by not making me do any extra work. As someone new into finance and accounting, simply showing me awesome graphs and telling me to save more on eating out next month is just not enough to motivate me to do so.

The approach with Debit & Credit might seem tedious to some but I would rather describe it as active finance management (over passive which mint offers). We tend to do better at things we do more actively, and give better attention to. By Debit & Credit being more active, I mean I have to enter each transaction into my transaction history without relying on an integration to pull all of that data from my banking accounts. In doing so, I started to see my spending patterns, and figuring out the recurring expenses that I could schedule to update into my statement as needed.

Being active should not mean I cannot automate some of the transactions, it just means I am more aware of when a transaction goes in or out. This experience of deciding when transactions come in or out of your transaction history gives you a lens into your financial future and past that you wouldn’t otherwise get with an application like Mint in my opinion.

Applications like Truebill make money off the fact that people do not know what goes in or out of their account. By paying a closer attention to this, you can offer yourself more of what Truebill offers by questioning all your outgoing transactions to see if they can be any less than they currently are. This new awareness will help you question things that services like Truebill would not even be capable of detecting. An example: A lot of web developers joke[1] about the number of domains they buy for potential side projects that never yield to anything. I add subdomains to my one domain instead because it not only does not give me an extra expense, it saves me from setting up a scheduled transaction for it. I have reversed how I put my laziness to use as my reluctance to track extra expense helps me avoid the irrelevant ones.

Redirect your reluctance for manual transaction tracking into a reluctance for creating irrelevant expenses that are not worth tracking.

As I used Debit & Credit more, and relished the predictability of income and expense, it made me see the importance of budgeting. With budgets, I can now have things that are typically not recurring expenses to become recurring when boxed up in a budget. In doing so, the monthly deficit or surplus become easy to derive, and this helps us as a family make attainable goals. I will share a spreadsheet template that links goals to cash flow below.

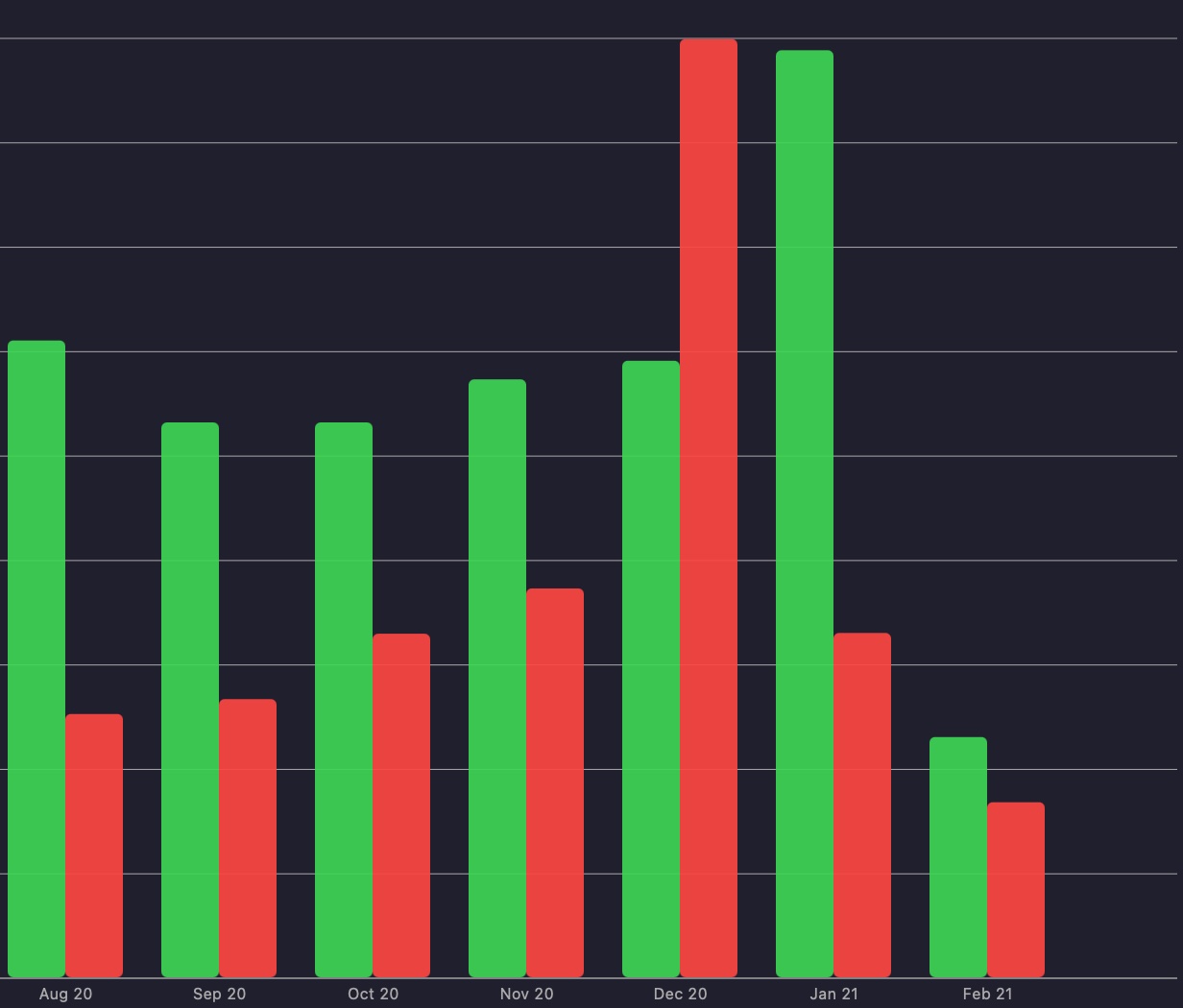

With all of the information we now have from entering our transactions, Debit & Credit provides some beautiful graphs too, making me not feel left out from a tool like Mint. It provides reports for theses:

In the How much do I earn compared to my expenses report, I can see the months with surplus and work towards either retaining that consistent surplus or working towards more. There are unfortunately a few months that deficits happen, but that should not be the leading trend.

To track these in a spreadsheet, you can use my template here (Disclaimer: this does not mirror my personal/family finance in any way).

I would love to go into how I have been able to apply some of the knowledge from this app into creating the super helpful spreadsheet with great formulas that I just shared with you, but I will dive into that in a different post.

It’s not a joke, people really have up to 100 domains they do not use and the average cost of one is $14 ↩︎